Resources

Freelancers Still Have Time to Apply for PPP Loans

By Rob LeDonne April 14th, 2021As a self-employed writer whose business was severely impacted by the pandemic, I was shocked when my accountant broke the news: I was eligible for a loan through the Paycheck Protection Program (PPP).

What seemed too good to be true turned out to be a financial blessing. And thanks to the recent passage of the PPP Extension Act of 2021, freelancers now have until May 31 to apply for their share of the approximately $68 billion left in the coffers at this time of this writing.

“It’s been a very busy time just staying on top of all of the changes and new laws,” said Lisa Greene-Lewis, a Certified Public Accountant (CPA) and tax expert at TurboTax. “People have had a lot of questions. As soon as new guidance from the IRS comes out, we’re translating the laws to see what they mean for our customers.”

PPP loans and other types of pandemic-related aid can seem nebulous since they’re still evolving. Demystifying the application process takes a bit of research and professional help. For those who had that same towering question that I had—“Am I eligible?”—Greene-Lewis has a clear answer. And for some of you, it’s welcome news.

Who can apply for PPP loans?

If you’re self-employed, whether as a career freelance writer or a professional juggler, congratulations! PPP loans are meant for people like you.

“Just about any small business owner qualifies for these loans,” Greene-Lewis explained. “Sole proprietors and independent contractors are all eligible. And if you’re a not-for-profit, the second package now includes you too.”

There are a few qualifications self-employed freelancers need to meet before filling out an application for a first-draw loan:

- You must have been in business on or before February 15, 2020.

- Your principal residence must be within the United States.

- You must have filed or plan to file a Form 1040 Schedule C for 2019.

- You must have had a net profit in 2019.

If you already received PPP funds, second-draw loan applications must also demonstrate a 25 percent reduction in revenue from 2019 to 2020.

There’s one last caveat: “Unfortunately, you can’t get unemployment [and PPP funding] at the same time,” Lewis-Greene said.

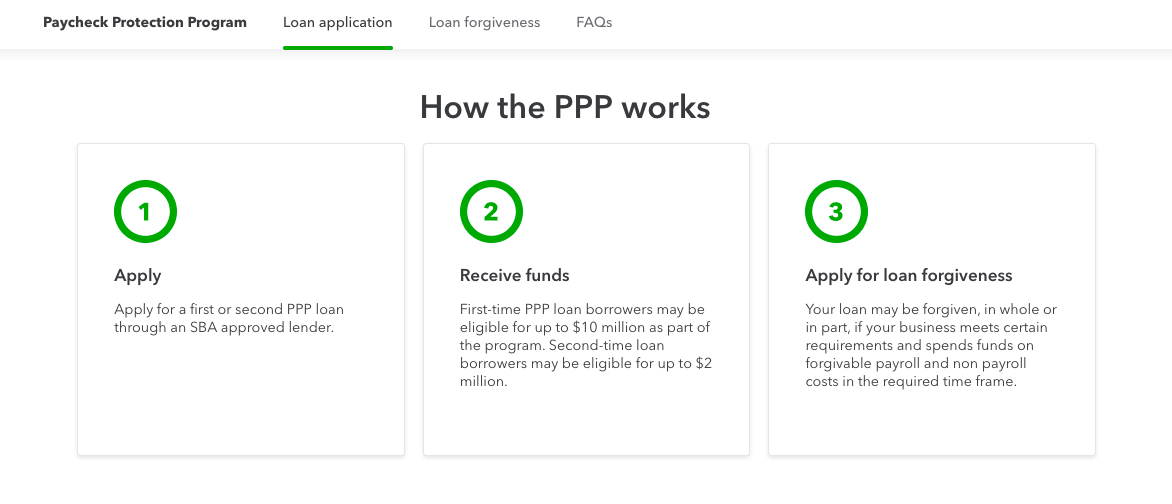

How can freelancers apply for PPP funds?

The next step is figuring out how to get your slice of the pie. If you’re working with an accountant, they’ll be able to guide you through the application process. If not, it’s as simple as visiting the Small Business Administration (SBA)’s website and finding a lender. The SBA can match you with an approved lender, or you can research the various options yourself.

Throughout this process, you’ll need some basic documents on hand, including proof you were in businesses before February 15, 2020 (a simple invoice will do); your 2019 or 2020 tax return; and any 1099-Misc forms from the same year. Some lenders may only require your Schedule C and proof of business operations, while others will ask for more detailed information. Your lender will let you know about any additional documents you’ll need to complete your application.

Now, the golden question: How much can you request? It all depends on your past tax returns and if you have any employees, but the max is 2.5 months’ worth of income.

To start, find line 7 of your 2019 or 2020 Schedule C—this is your gross income. Divide this number by 12, and then multiply by 2.5 to calculate the amount you’re eligible for. Recipients of Economic Injury Disaster Loan (EIDL) loans who wish to refinance may also need to factor in some additional calculations.

Although the biggest PPP loan a small business can request is capped at $2 million, compensation for sole-proprietors or independent contractors who operate without any employees is limited to an annualized salary of $100,000. So the the biggest loan you can get is $20,833.

How can freelancers get their PPP loans forgiven?

According to Greene-Lewis, once the check arrives, how most freelancers use it is up to them. In many cases, the funds fall into a category that’s considered “owner’s compensation replacement.”

“Yes, the funds can be spent to cover your personal salary,” Lewis-Greene said. “You can also pay for mortgages, rent or utilities for your place of business, or any other supplies and business-related expenses.”

Once you’ve spent your sweet influx of federal aid on any of the above, the good news is the loan is forgivable. But as Greene-Lewis is quick to point out, that part of the process isn’t guaranteed.

“You have to apply for forgiveness on the SBA website,” she said. “They may require some documentation and receipts showing what you paid for.” In other words, you may have a harder time getting a trip or vacation forgiven unless it directly relates to your work.

Will a PPP loan count as taxable income?

Another foreboding question PPP recipients might have is whether or not the loan is considered taxable income. After all, you are using it cover income, right? Might the federal government want to collect some of that cash back?

“When you receive a loan and you’re paying it back, it’s not taxable income for you in any way,” Greene-Lewis said. “The same is true here.”

Whether you’re just applying or still have questions, don’t beat yourself up if the PPP loans seem complex. The constant evolution of these loans is enough to make anyone frazzled. As always, be sure to research the latest guidance or ask a tax expert like I did.

“A lot of these provisions can change as time goes on,” Greene-Lewis said. “We’re constantly checking on the guidance every day.”

*Disclaimer: This content is for general educational purposes only. We are not financial advisors, and the information here is not intended to provide specific legal or tax advice for any individual.

Image by filo